The Market vs. Real Estate: Why It’s Time to Rethink Where You Park Your Wealth

Have you been watching the market lately? If you’re like most Americans with a 401(k), IRA, or brokerage account, chances are you’ve felt the sting of volatility. Between inflation, economic uncertainty, geopolitical instability, and policy whiplash from changing administrations, the stock market has become a rollercoaster ride that most can’t afford to stay on, especially those approaching retirement.

In the past 60 days, the stock market has experienced significant turbulence:

- April 3, 2025: The Dow Jones Industrial Average dropped 1,679 points (4%), and the S&P 500 fell 4.8% due to new tariffs announced by President Trump .wsj.com+14apnews.com+14nypost.com+14

- April 4, 2025: The Dow plunged another 2,231 points (5.5%), marking the largest two-day point drop in history .investors.com+4en.wikipedia.org+4nypost.com+4

- April 10, 2025: After a brief rally, the Dow fell over 1,000 points (2.5%) as uncertainty over tariff policies persisted .en.wikipedia.org+5nypost.com+5investopedia.com+5

- April 21, 2025: The Dow declined 972 points (2.5%) amid escalating trade tensions and criticism of the Federal Reserve .finance.yahoo.com+7foxbusiness.com+7investors.com+7

- May 21, 2025: The Dow dropped over 800 points (1.6%) as bond yields surged and deficit concerns grew .investopedia.com+1theaustralian.com.au+1

These events highlight the market’s volatility and the challenges investors face in such an unpredictable environment.

Meanwhile, real estate keeps doing what it has always done: grow in value, generate income, and offer powerful tax advantages. The average American may not have the time, knowledge, or risk tolerance to master the stock market, but we all understand real estate. Why? Because we live it.

It is a lived experience. Not a sales pitch about possible benefits and future returns.

Real estate has demonstrated consistent growth and offers several real advantages:

- Leverage: Control a valuable asset with a relatively small down payment.

- Tax Benefits: Deduct mortgage interest and property taxes.spglobal.com

- Appreciation: Historically, real estate appreciates over time.

- Rental Income: Generate steady cash flow from tenants.

- Tangible Asset: Unlike stocks, real estate is a physical asset you can use or improve.

Also, you have to ask yourself, especially given your financial position and life situation, is it worth the risk? Let’s look at the numbers.

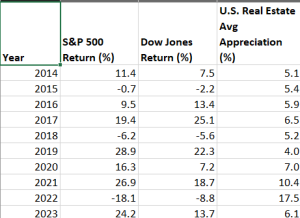

10-Year Annual Returns: Stocks vs. Real Estate

While the stock market has seen big swings—both up and down—real estate appreciation has remained positive and consistent, even during downturns. But that’s just the beginning of the story. Let me go deeper on the benefits.

The Hidden Power of Real Estate: Six Unmatched Advantages

Even if the returns were the same (they’re not), real estate would still win because of the following advantages:

1. Leverage

With real estate, a first-time buyer can control a $500,000 asset with as little as 3% down. That’s $15,000 controlling an appreciating half-million-dollar asset. In contrast, $15,000 in the stock market gets you… $15,000 in the stock market.

2. Tax Deductions on Mortgage Interest

Homeowners can deduct the interest on their mortgage from their taxable income—lowering their tax bill significantly. You can’t do that with stocks.

3. Deferred Capital Gains

Stock market gains are taxed when sold. Real estate gains are tax-deferred until the sale—and even then, a 1031 exchange allows you to defer taxes further by reinvesting into another property.

Clarification: You cannot write off capital gains tax in the stock market the way you can offset income in real estate. Capital gains tax is owed upon sale unless you’re selling in a tax-advantaged account (like a Roth IRA). Otherwise, it’s a direct hit.

4. Access to Equity Without Selling

Homeowners can borrow against their property through a HELOC or cash-out refinance—often at lower rates than securities-backed loans. Stocks? To access the money, you have to sell—and trigger taxes.

5. Personal Use + Schedule A Deductions

You can live in your investment. That means housing cost savings plus the ability to write off taxes, mortgage interest, and certain maintenance costs. Try doing that with Tesla stock.

6. Tangible Income Through Rent

For investment properties, real estate delivers a second stream of returns: cash flow. You benefit from appreciation and monthly rent. With proper management, tenants pay your mortgage while you build wealth.

BONUS: Security

Stocks can go to zero. Companies go bankrupt. A home? It may burn down or flood, but insurance rebuilds it. Real estate is permanent. It’s a shelter. It’s land. It’s the ground under your feet.

The Reality of Most Americans

Don’t let stock market millionaires fool you, they are the exception, not the rule. According to IRS and Census data:

- The average American makes around $60,000/year

- 50 to 60% of Black and Brown Americans and 30 to 40% of White and Asian Americans do not own a home

- Most Americans have little to no savings

- Credit scores range between 640–680

- A majority live paycheck to paycheck

And yet, Wall Street keeps preaching a gospel that most Americans can’t afford to follow or believe in.

My Recommendation. Move Your Money Now, While You Still Can. Look again at the headline news.

These aren’t hypothetical. These are the headlines. This is your portfolio we’re talking about:

- January 22, 2025: S&P 500 closed near a record high, driven by a tech rally fueled by AI enthusiasm and strong Netflix earnings (Reuters).

- January 31, 2025: Dow ends January up 4.7% despite a volatile final week (Investopedia).

- February 21, 2025: Dow plunges over 700 points on fears of economic slowdown—worst day of the year so far (NY Post).

- March 3, 2025: S&P 500 falls 1.8%, Nasdaq 100 down 2.6% after President Trump announces steep new tariffs on Canadian, Mexican, and Chinese goods (Investopedia).

- April 3, 2025: Dow plunges 1,679 points (4%), and S&P 500 falls 4.8%markets shocked by Trump’s tariff rollout (Wall Street Journal).

- April 4, 2025: Dow plunges another 2,231 points (5.5%)—largest two-day point drop in market history (MarketWatch).

- April 10, 2025: After a short-lived rally, Dow drops 1,000+ points again amid policy uncertainty (Investopedia).

- April 21, 2025: Dow falls 972 points (2.5%) as trade wars escalate, and Trump criticizes the Fed (WSJ).

- May 21, 2025: Dow drops over 800 points (1.6%) as bond yields spike and federal deficit concerns mount (Investopedia).

- May 30, 2025: S&P 500 and Nasdaq close their best month since November 2023 despite tariff turbulence (AP News).

- June 3, 2025: Nasdaq erases year-to-date losses; S&P and Dow gain as tech leads the rally (MarketWatch).

These events underscore the intense volatility of the market. If you’re in your 50s or 60s—or even late 40s—and nearing retirement, you must ask yourself: is this where your money belongs?

Let’s get into what to do about it…

If your market losses are in the 10% range, consider that a win exiting now—before they grow deeper. Now I know you don’t lose until you sale, but this is not about timing the market. This is about being in the market in the first place at this time in your life. Convert your 401(k) or IRA into a self-directed account and invest in real estate. Yes, you may pay some fees. Yes, there are rules. But yes, you will be securing your financial future with something you can live in, rent out, improve, and pass down.

You were born in real estate.

You grew up in real estate.

You work in real estate.

You’ll be buried in real estate.

You grew up in real estate.

You work in real estate.

You’ll be buried in real estate.

So why is your money not in real estate? Here are some common objections I hear:

“I can’t afford to invest in real estate.”

Consider starting with a smaller property, 4-unit property and live in one of the 4 units or partnering with your family and friends to purchase a home or investment. Consider buying an investment property in states where homes are very inexpensive. I published a HUD Homes magazine that is full of great deals in California. There are also financing options and programs for first-time buyers. You can start a syndication or Go fund me with family and families. You own what you manifest. Remember that.

“The stock market offers higher returns.”

While stocks can offer high returns, they come with higher volatility. Real estate provides more stable, long-term growth with additional benefits like rental income and tax advantages. Also, no none should have money in the market they cannot afford to lose. Full Stop. That is everyone. If you are in the market, you need to take out what you can’t afford to lose now. The market is a rich man’s game who has discretionary funds they can afford to lose. So are retirement accounts. If you do not have an emergency fund of 12 months of your income you should not be invested in any investment account of any type. Not even a 401k. What happens if you need the money? Need I say more. It’s like owning a gun and keeping it safe instead of carrying it. You will not have access to it when you need it the most.

“Real estate requires too much management.”

Property management companies can handle day-to-day operations, allowing you to enjoy the benefits without the hassles. In addition, you do not know the landlord laws and requirements. Leave it to the professionals or you risk fines, loss of rent and maybe even the loss of your property.

Conclusion

Given the recent market volatility, it’s prudent to consider diversifying your investments. Real estate offers stability, tangible assets, and multiple income streams.

If you’re interested in exploring real estate investment opportunities, feel free to reach out for guidance tailored to your financial goals. If you are a seasoned homeowner or investor sitting on a bunch money this blog is not for you. Ride the market out. You can afford the risk. You are a 1% percenter. Congratulations. But for the rest of you, heed my advice. Get out now if you can.

It’s time to stop hoping your retirement grows while riding the waves of the market. Take control. Build equity. Build multiply streams of rental income. Reclaim control of your future.

If you need help making the transition, I can guide you through it.

Thank you for reading this blog. I appreciate your continued support in raising awareness about the issues that impact our communities the most. Please share this blog—and explore my other articles and videos—each one created to educate, empower, and uplift. Together, we can challenge the systems that hold us back and push forward policies that open the doors to opportunity for all.

Eric Lawrence Frazier, MBA

Your trusted advisor in business and wealth

www.ericfrazier-com-869976.hostingersite.com | www.thepowerisnow.com

NMLS #451807 | CA DRE #01143484

Schedule a consultation: https://calendly.com/ericfrazier/real-estate-mortgage-consultation-clients

Your trusted advisor in business and wealth

www.ericfrazier-com-869976.hostingersite.com | www.thepowerisnow.com

NMLS #451807 | CA DRE #01143484

Schedule a consultation: https://calendly.com/ericfrazier/real-estate-mortgage-consultation-clients